Debt: Amplifier of Strength — or Fragility?

Why the structure behind borrowing matters more than the interest rate

Only a few weeks ago, the conversation was about relief.

Inflation appeared to be moderating. Interest rates looked as though they might begin easing and the recent Budget Speech spoke about supporting economic growth. Things were looking up.

Then, almost overnight, conflict in the Middle East escalated and suddenly markets are once again debating inflation risks, rising oil prices and the possibility that monetary policy may need to remain tighter for longer.

This is the reality of the world we live in. Conditions can change in an instant. Tonight we go to sleep and tomorrow we wake up to WWIII.

And when they do, the question that matters most is not what interest rates are doing today, but whether the financial structures we have built can withstand tomorrow.

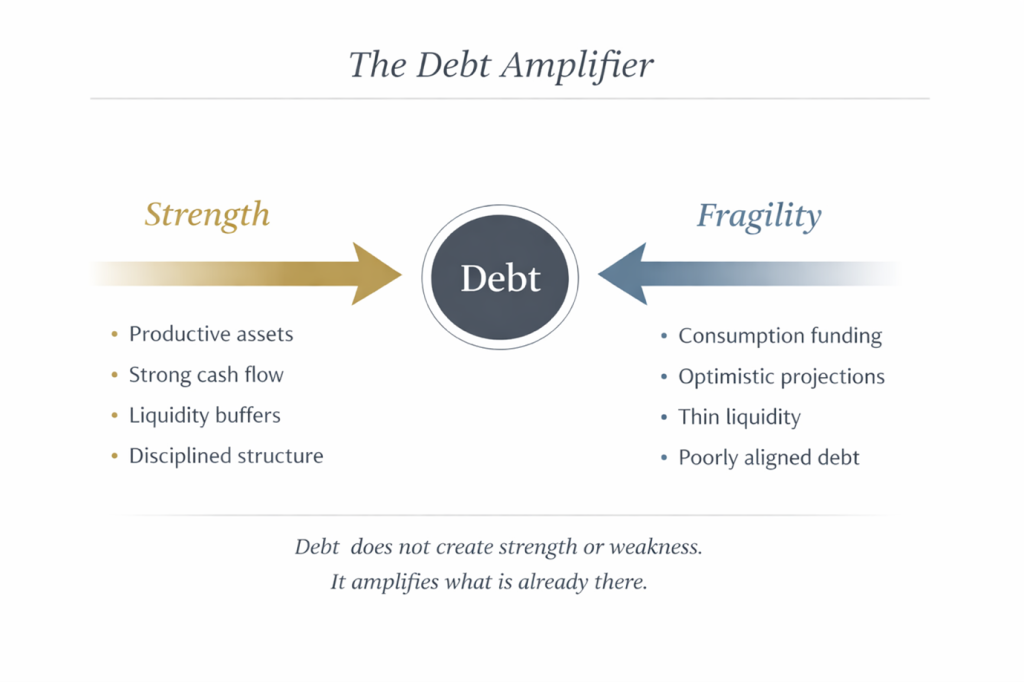

This is where debt reveals its true nature. The reason is that debt behaves very differently depending on the structure beneath it. The same leverage that builds wealth in one environment can destroy it in another. The same facility that funds growth, can become the pressure point that collapses a balance sheet.

And yet we still tend to talk about debt as if it were a moral issue. Good debt.

Bad debt. But debt itself is neither virtuous nor reckless. It is structural. It either strengthens a balance sheet or exposes weakness.

And in uncertain times, structure matters more than ever.

WHAT DEBT ACTUALLY DOES

Debt pulls capital forward in time. It allows you to acquire an asset, expand a business, fund strategic investment or diversify exposure without first accumulating the full capital required.

Leverage is an amplifier. It magnifies returns, it magnifies mistakes and it accelerates outcomes, in both directions!

Over the years, working as a debt structurer and balance sheet optimiser, I have learned that the real risk in borrowing is rarely the interest rate. It is the structure.

For much of my career I sat between clients and credit committees, designing facilities that could withstand volatility rather than simply get approved. The discipline was never: “How much can we get approved?” (well actually never is a strong word) It was “Will this structure survive under stress?”

That distinction matters.

THE DISCIPLINE OF STRESS TESTING

In my career, I have lived through two severe upward interest rate cycles. They were not gradual, but more like that roller coaster at Disneyland that keeps going up and up into the night sky. Instalments moved quicker than the twists and turns on the way down and liquidity tightened quicker than the ride came to an end. Structures that once appeared comfortable suddenly became distressed.

Then COVID brought a different kind of shock. Not rising rates, but income disappearing literally overnight. Even strong businesses faced months with little or no revenue. Those that became super creative thrived despite the odds. I can’t help thinking we all thought our next career would be in pineapple beer or banana bread manufacture!

In both cases, debt itself was not the root problem. The absence of a back-up plan was. Insufficient stress testing. We now know, you need to stress test for the scenarios that couldn’t possibly ever exist!

Before any borrowing decision, I insist on modelling two uncomfortable scenarios:

- A dramatic upward shift in interest rates

- A material drop, or complete dry up, of cash flow and of income

If the structure cannot survive both, it is fragile. That discipline is not pessimism.

It is stewardship.

In practice, responsible borrowing usually comes down to a few disciplined questions.

THE FOUR QUESTIONS I ASK BEFORE STRUCTURING DEBT

Over the years, when helping families and entrepreneurs structure borrowing responsibly, the conversation usually comes down to four fundamental questions.

- What is the purpose of the debt?

Is it funding a productive asset, strengthening a balance sheet or simply supporting consumption?

- Can the cash flow withstand stress?

Not just today’s instalment, but a dramatic rise in interest rates or a meaningful drop in income.

- Is the asset and liability properly aligned?

Currency, duration and liquidity all matter.

- Does the structure preserve optionality?

Strong balance sheets retain flexibility when conditions change.

These questions are rarely complex, but answering them honestly often determines whether debt becomes a tool for growth or a source of pressure when conditions change.

WHEN DEBT IS STRUCTURALLY WISE

Debt can be highly effective when aligned with purpose and capacity.

It can:

- Fund expansion of profitable enterprises

- Acquire productive property aligned to long-term strategy

- Preserve liquidity while investing

- Enable offshore diversification

- Assist with estate planning

- Align currency exposure appropriately

- Optimise certain tax outcomes when structured correctly

Tax efficiency should support the strategy, not drive it. If the structure lacks resilience, tax efficiency will not rescue it.

OFFSHORE DEBT AND STRATEGIC OPTIONALITY

For families with global assets, offshore borrowing can be a useful strategic tool.

Matching offshore liabilities with offshore assets can reduce currency mismatch risk. Funding international investments without unnecessary local asset sales can preserve liquidity.

Again, the principle remains the same: alignment, capacity and discipline.

DEBT CEILINGS AND GOVERNANCE

The discussion around a potential national debt ceiling is ultimately about discipline. A borrowing limit can provide guardrails and reinforce fiscal responsibility, but a ceiling without coherent growth strategy can also constrain productive investment.

At a national level, just as at a family level, the real question is not whether debt exists. It is whether borrowing is governed with discipline and aligned with long-term objectives.

THE EVOLUTION OF CREDIT MARKETS

Traditional banks have become increasingly conservative in their lending frameworks. Frankly, with what has happened in the past 5 years and before, I cannot say I am surprised. It has however created opportunities and is one reason the private credit industry has expanded so rapidly. Many borrowers today are willing to pay a slightly higher interest rate simply to avoid lengthy administrative processes and slow approval timelines.

Private lenders can offer flexibility. The concern is that much of this capital sits outside the regulatory frameworks that govern banks.

And every credit cycle eventually tests its weakest structures. Access to capital is not the same as capacity for capital.

THE UNCOMFORTABLE REALITY OF AN UNCERTAIN WORLD

We live in a world where economic conditions can shift very quickly. Just when consumers begin to feel relief, perhaps through stabilising interest rates, a geopolitical event (think missiles and oil!) can change the outlook overnight.

The recent escalation of conflict in the Middle East is a reminder of how quickly inflation expectations can shift. Energy prices rise. Petrol prices move higher. Central banks reassess policy.

Debt structures designed only for stable conditions rarely survive unstable ones.

With the right advice, appropriate leverage levels and disciplined structuring, these storms can be weathered, but only if the structure was built with volatility in mind from the start.

In my experience, the structures that survive uncertainty are rarely the most aggressive. They are the most disciplined.

A CALL I WILL NEVER FORGET

Years ago, I worked with a client whose business had become distressed. The banks were preparing to foreclose.

We restructured the debt, extended maturities, renegotiated terms, rebuilt liquidity buffers and imposed disciplined cash management.

It was uncomfortable. But he kept everything.

Years later, long after I had moved on from that organisation, my phone rang. It was him. He had just made the final payment on the restructured debt.

In that moment I realised something important.

Debt had almost taken everything from him. But belief, structure, discipline and time had restored it.

THE CURRENT MOMENT

If interest rates decline, borrowing will feel easier. If policy signals support growth, confidence may improve. But a falling rate cycle is not permission. It is an opportunity if the structure and rationale is sound.

Debt is powerful. Used wisely, it can accelerate growth, preserve capital and strengthen intergenerational plans. Used carelessly, it can destroy decades of hard work in a single cycle.

Debt is not the enemy. Poor structure is.

The real question is not: “Should we borrow?” It is: What are we building and will the structure survive the next storm?

For more than two decades, my work has centred on helping families and entrepreneurs structure balance sheets that can withstand uncertainty, aligning assets, liabilities and long-term objectives with discipline and clarity. Because when the next storm inevitably arrives, structure is often the difference between resilience and regret.

And in finance, as in life, the structures that endure are rarely the most aggressive. They are the most thoughtful.